Why Every Hard Asset You Hold Today Is Irreplaceable on a Salaried Income — and Why Selling One Is a One-Way Door

There is a scene that exists in virtually every Indian film made between 1960 and 1970s.

The setting changes — a village courtyard, a zamindar’s haveli, a moneylender’s office. But the man is always the same: a father, broken and trembling, reduced to begging. And the line he delivers, through tears, is some version of this:

“Sarkar, I have nothing. But I have kept 20 tolas aside for my daughter’s wedding. I beg you — please don’t take that.”

That was the floor. Twenty tolas was what a broke, desperate, rock-bottom man in rural India considered the absolute minimum his daughter deserved. It was not wealth. It was the last line of dignity.

Now consider the present.

Today, a dual-income household — both partners with engineering degrees, both drawing salaries that would have seemed fictional in that film — cannot accumulate 20 tolas. Not because they do not earn enough. Because every rupee they earn is pre-mortgaged before it arrives: the home loan EMI, the car payment, the phone upgrade on credit, the personal loan taken to cover last year’s shortfall.

The poor man in that film had 20 tolas set aside. We have a CIBIL score and a subscription to a budgeting app.

This article has one purpose: to tell you, clearly and without softening, that once you sell hard assets such as gold jewellery, inherited land, or property, you are unlikely to ever buy back gold jewellery or replace those assets on a salaried income. The mathematics of the modern economy make it structurally impossible for most families. What feels like a temporary solution is almost always a permanent loss.

If you are reading this because you are considering selling a hard asset to solve a financial problem, read this first. All of it.

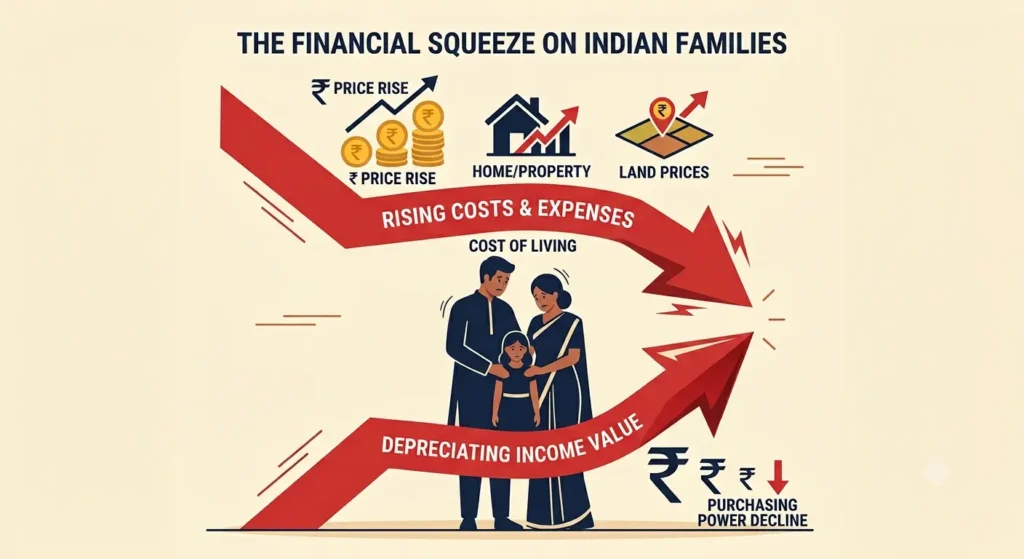

We Earn More Than Our Parents. We Own Less.

The numbers are not in dispute. In nominal terms, the current Indian middle class earns far more than any previous generation. A software engineer’s monthly salary today would have been a comfortable annual income for their father. A government employee’s take-home pay has risen twenty-fold since 1990.

And yet, run a simple comparison. What did that income actually buy in terms of real, tangible assets?

17.9x National housing affordability index — An average Indian family needs 18 years of total income just to buy a home (2025 data)

61% Home loan EMI as % of income — Up from 46% in 2020 — the global red-flag threshold is 50%

+10–24% Urban home prices, Noida / Gurugram — Rise in a single year, 2025–26

Our parents bought homes on single salaries when the price-to-income ratio in most Indian cities was under 4. They accumulated gold through wedding gifts and modest annual savings. They owned agricultural land transferred across generations without a bank involved.

We pass more money through our hands in a month than they saw in a year. But the assets — the things that hold and grow wealth across time — have inflated so far beyond salary growth that the gap is now structural, not temporary.

We are not going to earn our way back to where they were. We are running faster on a treadmill that is accelerating.

Priced Out of Everything: Not Just Homes and Gold

The asset squeeze is wider than most people acknowledge. Think about what the generation before us possessed without debt, without financial planning, without deliberate sacrifice:

- A home — modest, perhaps two rooms, but fully owned. No bank. No 20-year obligation.

- A piece of land — a family plot, an agricultural holding, or a small backyard. Something physical, unencumbered, theirs.

- A tree — a coconut, a mango, a neem. Planted on their own ground. Producing food and shade at zero cost, every year, without fail.

- Water — from a well, a shared source, a municipal tap that actually worked. It arrived without a monthly bill. Today, the average urban household pays for packaged drinking water, a purifier on the kitchen wall, and in many apartment complexes, a water supply surcharge on top of maintenance fees.

- Gold — not bought as an “investment strategy” but accumulated naturally: a little at each wedding, a little at each harvest, a little saved each year without thinking much about it.

Every single item on that list has been commodified and placed behind a financial barrier that rises every decade. Water is now a product with a price tag. Trees require land that costs crores. A home requires a lifetime of debt servitude. Gold requires sustained financial discipline that the modern economic machine is specifically designed to undermine.

We now pay monthly for water our grandparents drew from a well. We earn ten times more and own ten times less of the real, permanent world.

The System Moves You Away from Ownership — by Design

Every financial nudge in the modern economy pushes you away from holding physical assets and toward renting, subscribing, and holding paper:

- Rent your home rather than own it — “flexibility” is the pitch; the landlord builds equity while you build nothing.

- Book an Uber; subscribe to your software; pay for your water by the can.

- Hold paper gold, ETFs, and digital units rather than physical metal — where your wealth stays inside someone else’s system, subject to their platform risk, their management fees, and their ability to settle in cash rather than metal.

Physical, tangible assets held directly — gold in hand, land with your name on the deed, a property you actually occupy — are the one category of wealth that exists completely outside this system. They cannot be printed, suspended, hacked, charged a fee, or settled in depreciating paper.

This is precisely why every institutional incentive steers you away from them. And it is precisely why every family that holds them should understand what they are actually holding: a position in the shrinking space of things that are still possible to own.

Can You Buy Back Gold Jewellery or assets Once Sold?

In every jeweller’s shop, every land registration office, every property broker’s cabin, you will find families in the process of selling an asset under pressure. And you will hear some version of the same sentence from almost all of them:

“It is temporary. Once this passes, we will buy it back.”

Across gold, land, and property — this promise is almost never kept. Not because families lack intention. Because the mathematics work against them from the moment the asset leaves their hands.

- The cash received is at its maximum purchasing power the moment it arrives. Inflation erodes it from that second onward, silently and without pause.

- The hard asset sold will, in virtually every historical scenario, be more expensive in three, five, and ten years. Finite physical assets appreciate in fiat currency terms. That is not a theory — it is the recorded history of gold, land, and property in India across every decade.

- The funds received are absorbed entirely by the crisis that triggered the sale. Nothing is left to rebuild with.

- Life does not pause while you recover. New EMIs, new obligations, new emergencies arrive before the savings plan can begin.

The family ends with neither the asset nor the financial surplus. Only a resolved crisis — and a permanently weakened foundation that silently worsens with each passing year.

Every family that has ever sold hard assets in a crisis has told themselves it was temporary. Ask them ten years later.

The Arithmetic of Recovery: You Must Be Far More Successful Tomorrow

This is the section most financial articles avoid because the numbers are uncomfortable. So let us be direct.

Suppose a family sells 25 tolas of 22-carat gold today at approximately ₹1.45 Lakhs per tola. After the standard 15–20% deduction for making charges, wastage, and GST, they net around ₹30 Lakhs. That money goes to the purpose it was sold for — a debt, a medical bill, a business shortfall.

Now: what does buying that 30 Lakhs worth gold back actually require?

₹90 Lakhs+ Buyback cost in 10 years — At 8% annual gold appreciation (conservative), including charges and GST.

₹1.7 Crore+ Buyback cost in 20 years — Same 25 tolas, same compounding rate.

Whereas ₹30 Lakhs Amount received at sale — After all deductions — a 3x to 6x gap to close.

The same logic applies to land and property. A plot sold in this year to fund a crisis will cost two to four times as much to repurchase after ten years. A flat liquidated today will require a different family’s lifetime savings to buy back after twenty years.

The implication is not subtle: to earn back what you sold today, you must not return to your current financial level. You must achieve a level three to five times greater — in an economy that will be more competitive, more expensive, and more demanding than today’s.

And this assumes no further crises between now and then. No job loss, no health emergency, no second financial shock. For most Indian families, that assumption is not realistic.

Selling a hard asset is not stepping back one rung on the ladder. It is stepping off the ladder entirely, and then being asked to build a new one that is three times taller.

Inflation: The Attack That Comes from Both Sides

Inflation does not merely push the price of your target asset higher. It attacks from two directions at once, and both work against you simultaneously.

On one side: the cash you received loses purchasing power every single day it sits in your account. At 6% annual inflation, ₹30 Lakhs today is worth approximately ₹22 Lakhs in real terms after six years. The money is disappearing even as you plan to use it.

On the other side: gold, land, and property — all priced in fiat rupees — appreciate in rupee terms precisely because the rupee is losing value. This is not speculation. It is the mechanical relationship between currency depreciation and hard asset prices that has played out in India in every decade of recorded data.

The result: you are running on a downward escalator toward a door that is moving upward. Every year of delay between selling and attempting to rebuy widens the gap. After five years, recovery is very difficult. After ten, it is nearly impossible on a salaried income. After twenty, it simply does not happen.

Why the Economy Rewards Those Who Hold and Punishes Those Who Sold

Here is the structural reality that makes all of the above so difficult to escape. The modern economy rewards ownership over income — not marginally, but substantially and increasingly.

If you hold physical gold, agricultural land, or residential property, those assets appreciate while you sleep. You receive a second income — not from labour, but simply from the asset existing in your name. This is the mechanism by which existing wealth compounds automatically.

If you have been forced to sell your hard assets, you are left with salary income alone. Every rupee of wealth must be earned through active work, competing daily against millions of other earners in a job market that grows more demanding every year.

The result is a structural divergence: those who hold assets accumulate further wealth through appreciation. Those who have sold are trapped on the treadmill of active income, watching the prices of the assets they want to recapture move further out of reach with every passing year.

This is what it means when people say the economy is increasingly skewed toward the successful. It is not about ambition or qualifications. It is about whether you hold appreciating assets that compound on your behalf — or whether you trade only time for money.

The One Exception: Swapping One Hard Asset for Another

Everything argued above applies to one specific scenario: selling a hard asset to fund consumption — clearing debt, covering bills, bridging a business loss, or paying for an event. In that case, you are exchanging an appreciating physical asset for fiat currency that will be spent. The asset is gone. The money follows.

There is a fundamentally different scenario that deserves to be treated separately: selling one hard asset to acquire a better or more suitable hard asset. This is not liquidation. It is conversion.

- Selling gold ornaments or jewellery as part of the down payment for a house. You are moving from one hard asset — portable, liquid gold — to a different hard asset — immovable, appreciating real estate that also provides shelter security. Your family’s hard-asset foundation is not diminished. It is transformed and, in most urban markets over a 10-year period, likely strengthened.

- Selling a plot to purchase family gold or heirloom jewellery held with clear long-term intent. An unproductive plot, especially with unclear title, legal complications, and no income may rationally be converted into gold that is portable, clearly owned, easily passed to the next generation, and liquid in any emergency.

The test in both cases is the same and simple: are you staying inside the world of hard assets, or are you leaving it?

If you are converting one real asset into another of comparable or greater long-term value, you are making a wealth-management decision. Your family remains anchored.

If you are converting a hard asset into rupees that will be spent — on a car loan, a wedding beyond your means, a failing business, or any form of consumption — you are making a permanent withdrawal from the only financial safety net your family has.

Selling gold to buy a house is swapping one anchor for another. Selling gold to pay for the wedding reception is trading your family’s permanent security for a one-night memory.

The Hidden Costs: Why Even a “Same Year” Buyback Fails

Even before accounting for any price appreciation, the mechanics of selling and rebuying a hard asset are stacked heavily against you. Most people do not calculate this until it is too late.

- When you sell gold, you take an immediate 15–20% haircut: making charge deductions, wastage, stone weight, and GST. You never recover the full metal value at the point of sale.

- When you sell land or property, capital gains tax, registration costs, and agent commissions typically remove 8–12% of the transaction value before you see a rupee.

- When you attempt to rebuy, you pay the new elevated price, plus GST, plus fresh transaction costs, plus all appreciation that has occurred in the interim.

- Every rupee you earn toward the buyback is taxed as income on entry, and taxed again on purchase on the way out.

The full round-trip cost of selling and rebuying the same asset within a single year is 25-30 % of the asset’s value in charges, fees and taxes alone — before any price appreciation is factored in. Extend the timeline to ten years and the mathematics are essentially irreversible for any salaried household.

The Only Situations Where Selling Is Genuinely Justified

This is not an argument that hard assets must be held under all possible circumstances. Genuine emergencies exist. Life is not a spreadsheet. Here is the honest framework:

Selling is justified:

- A genuine life-or-death medical emergency where no other liquidity source exists and the cost cannot wait.

- Preventing a financial collapse that would cost the family significantly more than the asset’s value — avoiding bankruptcy, a legal judgment, or loss of the primary income.

- Converting one hard asset into another of comparable or greater long-term value — selling ornamental gold toward a home purchase, or selling an unproductive plot to acquire more portable and clearly titled gold for the long term.

Selling is not justified:

- Consumer debt, credit card balances, or personal loans. These can be restructured, negotiated, or settled over time without touching assets.

- Funding a wedding, a celebration, or a social obligation beyond your genuine means.

- Propping up a failing business. Failing businesses consume capital without limit. The asset will be gone and the business will still fail.

- Lifestyle purchases: a new car, a home renovation, electronics, a foreign holiday.

- Transferring hard assets into paper investments with the intention of “buying back later.” That later rarely comes.

The test every time is the same: Am I converting one real asset into another? Or am I converting an irreplaceable physical asset into currency that will be consumed? The first is financial management. The second is almost always, in hindsight, the decision a family wishes it had not made.

Before You Touch the Assets: Exhaust Every Alternative

If you are facing the kind of financial pressure that makes the locker or the land documents look like the answer, work through this list completely before you act:

- Gold-backed loans: Banks and NBFCs lend 65 to 75% of gold’s market value at interest rates far lower than personal loans. The gold is held as collateral and returned in full when the loan is repaid. You solve the crisis and keep the asset.

- Loan against property: If you hold real estate, it can be used as security for a loan at 10 to 13% annual interest. You retain full ownership throughout the loan period.

- EMI restructuring: A single phone call to your existing lender can sometimes free up the cash flow you need. Most banks would rather restructure a loan than write it off. Ask.

- Liquidate depreciating assets first: Sell the car. Redeem the mutual funds. Exit paper positions. Touch physical hard assets only after everything else has been considered.

- Family lending: Short-term, zero-interest borrowing from within the family is available to many who skip it only because the conversation feels uncomfortable. It is not unavailable. It is just uneasy.

Hold What Cannot Be Replaced

We began with a scene from an old film. A desperate father, 20 tolas, and a plea not to take the last thing he had saved for his daughter’s future.

That man, by the standards of his time, was poor. He had no career, no salary, no credentials. But he had accumulated, through years of restraint and sacrifice, 20 tolas of gold that he considered non-negotiable. It was the floor beneath his family. The line he would not cross.

Today, that floor has been removed — not by poverty, but by the architecture of modern consumption. We earn more than he ever dreamed of. And we cannot hold that floor.

But some families still can. Some families still have the gold in the locker, the plot in the village, the property whose title is clean. If yours is lucky enough to be one of them, understand what you are holding. It is not just metal, or land, or a document. It is the accumulated sacrifice of the people who came before you, preserved in one of the few forms that survives inflation, survives market crashes, and survives the relentless pressure of modern life to convert everything into something spendable.

Once you sell it, recovery requires you to be, in ten years, three to five times more successful than you are today. In an economy that skewed against families and grows more expensive every year, with asset prices that compound faster than salaries, for most families that level of success will never arrive.

The hard asset you hold today is irreplaceable on a salaried income. That is not a warning. That is a mathematical fact.

Do not sell what you cannot buy back. And understand clearly: on a salary, you almost certainly cannot buy it back.

FREQUENTLY ASKED QUESTIONS

Is selling family gold jewellery a good financial decision?

Selling family gold jewellery may solve an immediate cash shortage, but it is rarely the best long-term financial decision. Once family jewellery is sold, it is often impossible to buy back the same pieces because of rising gold prices, making charges, and their sentimental and family value. Before selling, consider alternatives such as building an emergency fund, reducing expenses, or using other financing options.

Why can’t I earn back gold jewellery once I sell it?

Many people underestimate how difficult it is to earn back gold jewellery after selling it. Gold prices tend to rise over time, and buying new jewellery also involves making charges, taxes, and design costs. As a result, replacing the same amount of jewellery often requires much more money than you received from selling it.

Why should families protect hard assets?

Hard assets often provide financial stability during uncertain times. They can be passed on to future generations, appreciate in value, and serve as a foundation for long-term wealth. Protecting these assets helps families build financial resilience instead of relying solely on income.

Why can’t the Indian middle class accumulate gold, houses or any hard assets like the previous generation?

The previous generation bought homes and accumulated gold when the price-to-income ratio was under 4x. Today it exceeds 17x in most Indian cities. Combined with home loan EMIs, car loans, and rising consumer costs, even most dual-income households have no surplus left for hard asset accumulation — even on salaries that would have seemed extraordinary a generation ago.

Is selling gold to buy a house in India a good idea?

This is one of the few justified scenarios. You are converting one hard asset (gold) into another hard asset (property). Your family’s real-asset foundation is transformed, not depleted. The key test: are you staying inside the world of hard assets, or converting them to cash that will be spent?