Table of Contents

Introduction

Owning a home is one of the most massive financial commitments most Indian families will ever undertake. A house is not merely a paper asset on a balance sheet. It is the physical foundation where your family lives, grows, celebrates, and builds heritage across generations. Protecting that foundation is not just a maintenance expense—it is a responsibility.

Yet, many homeowners obsessively budget for their EMIs, insurance premiums, and utility bills while remaining completely blind to one unavoidable truth: the absolute necessity of saving for home repairs. A leaking bathroom, a failed water pump, a dangerous electrical fault, or a structural waterproofing issue rarely arrives at a convenient time. But let’s be brutally honest: the real problem is not the repair itself. The problem is the complete lack of financial preparation.

Saving for home repairs is one of the most severely overlooked financial habits in India—and easily one of the most critical. A dedicated home repair fund transforms these structural inevitabilities from full-blown financial crises into routine, manageable maintenance. Ultimately, wealth is not measured by the sheer size of your home. It is measured by your ability to maintain it without financial stress.

This guide explains exactly why repairs are inevitable, how much Indian homeowners should save, where to keep the money, and how to build a practical, bulletproof home maintenance fund.

Quick Answer: How Much Should You Save for Home Repairs ?

A practical rule is to save around 1% of your home’s value every year.

₹25 lakh home → ₹25,000/year (~₹2,100/month)

₹50 lakh home → ₹50,000/year (~₹4,200/month)

₹75 lakh home → ₹75,000/year (~₹6,250/month)

₹1 crore home → ₹1,00,000/year (~₹8,300/month)

Older homes, coastal regions, and high-humidity cities may require 1.5–2% annually.

Why Home Repairs Are Inevitable

Every house ages. It does not matter whether your home is a brand-new apartment in Hyderabad or a fifteen-year-old independent house in Coimbatore. The materials that make up your home — cement, pipes, waterproofing membranes, electrical wiring, wooden frames, ceramic tiles — all have a finite lifespan.

This is not a sign of poor construction. This is physics and chemistry at work over time.

Here are common repair needs most Indian homeowners will face over the life of their property:

- Water seepage and dampness in walls or ceilings

- Plumbing failures — leaking pipes, blocked drains, broken taps

- Electrical faults in wiring, switchboards, and distribution panels

- Water pump motor failure (motor burnout is common after 6–8 years)

- Air conditioner breakdown or compressor failure

- Waterproofing failure in terraces and bathrooms

- Floor tile cracking, lifting, or grout deterioration

- Paint peeling due to moisture, mould, or age

- Wooden door/window frames warping or rotting

- Overhead water tank cracks or contamination

A home is the single largest asset most Indian families will ever own. Protecting it requires proactive maintenance. And maintenance requires money that must be ready before the problem arrives — not scrambled for after.

The Monsoon Factor: A Uniquely Indian Repair Risk

| Why every Indian homeowner needs extra financial preparation : India’s monsoon season (June to September) is the single biggest driver of home repair costs in the country. Heavy rainfall, humidity, and waterlogging create damage that can silently worsen for months — and then arrive as a large repair bill after the season ends. |

The following repair triggers are directly linked to the monsoon season and are almost entirely absent from international home finance advice:

| Repair Type | Monsoon Trigger | Estimated Cost (₹) |

|---|---|---|

| Terrace/roof waterproofing | Rainwater penetration through aged coating | ₹15,000 – ₹80,000 |

| Wall seepage treatment | Water ingress through exterior walls | ₹8,000 – ₹40,000 |

| Drain and pipe unclogging | Debris blockage during heavy rain | ₹2,000 – ₹8,000 |

| Mould and fungus treatment | High indoor humidity over 3–4 months | ₹5,000 – ₹20,000 |

| Electrical short circuit repair | Moisture in junction boxes or panels | ₹3,000 – ₹25,000 |

| Door/window frame repair | Wood swelling and warping from moisture | ₹4,000 – ₹20,000 |

Pre-monsoon preparation — checking drains, applying waterproofing sealant, inspecting electrical insulation — typically costs ₹5,000 to ₹15,000 per year but can prevent repairs costing ten times that amount. Smart homeowners build this annual maintenance cost into their home repair fund.

The Problem With Waiting Until Something Breaks

Most Indian homeowners follow a reactive approach: wait for something to fail, then find money for it. This creates following serious financial problems.

Financial stress and poor decisions under pressure

When a large repair arrives without a fund behind it, you are forced to make decisions quickly and under stress. Contractors quote higher prices to panicked homeowners. You accept the first quote rather than comparing two or three. You choose cheaper materials to cut cost now, and pay more for a repeat repair in three years.

Draining your emergency fund

Your emergency fund is meant for income disruption — job loss, hospitalisation, a family crisis. When it gets used for a leaking roof, you deplete the buffer your family needs for true emergencies. You then spend the next 8 to 12 months rebuilding it, leaving yourself financially exposed during that period.

Delaying repairs until they become disasters

Without money available, many families postpone repairs. An ₹8,000 seepage treatment ignored today can become ₹60,000 of structural waterproofing work after two monsoons. What begins as a small damp patch can eventually damage paint, furniture, electrical fittings, and even neighbouring flats. In homeownership, the repair is rarely the most expensive part. The delay is. Small problems left unattended become expensive disasters

The Hidden Cost of Home Ownership Nobody Talks About

Most people focus on the visible costs of buying a home:

- Down payment

- Home loan EMI

- Registration charges

- Property tax

- Home insurance

But the true cost of home ownership does not end on possession day. Every home slowly consumes money through maintenance, repairs, replacements, and age-related wear. A bathroom waterproofing failure, a burnt-out water pump, an electrical fault, or post-monsoon seepage can arrive years after purchase—but they are still part of the cost of owning a house.

This is why many homeowners feel financially surprised even when they can comfortably afford their EMI. The bank finances the purchase of your home. Nobody finances its upkeep. That responsibility belongs entirely to the homeowner.

A house that costs ₹50 lakh to buy may require several lakhs of maintenance and repairs over its lifetime. Ignoring these future expenses creates a false picture of affordability. The real cost of home ownership is not just buying the house. It is maintaining the house for decades after you buy it.

Why Saving for Home Repairs Is the Smartest Financial Move You Can Make

Building a dedicated home repair fund changes your entire experience of homeownership. Here is what specifically changes:

- Financial surprises disappear. When a repair arrives, the money is already waiting.

- Your emergency fund stays intact for real emergencies.

- You avoid high-interest debt entirely.

- You can choose quality repairs — better contractors, better materials — rather than the cheapest available option.

- You make repair decisions from a position of calm, not panic.

- Your home holds its value because you maintain it properly.

Wealth is not measured by the size of your home. It is measured by your ability to care for it without financial stress.

| WealthDharma Research Note : Home repair costs vary widely across India. The estimates in this guide have been reviewed using information from homeowners, contractors, apartment associations, maintenance professionals, and market pricing across multiple Indian cities. Use these figures as planning estimates rather than exact quotations. Your actual costs will depend on your property’s age, location, construction quality, and the scope of work required. |

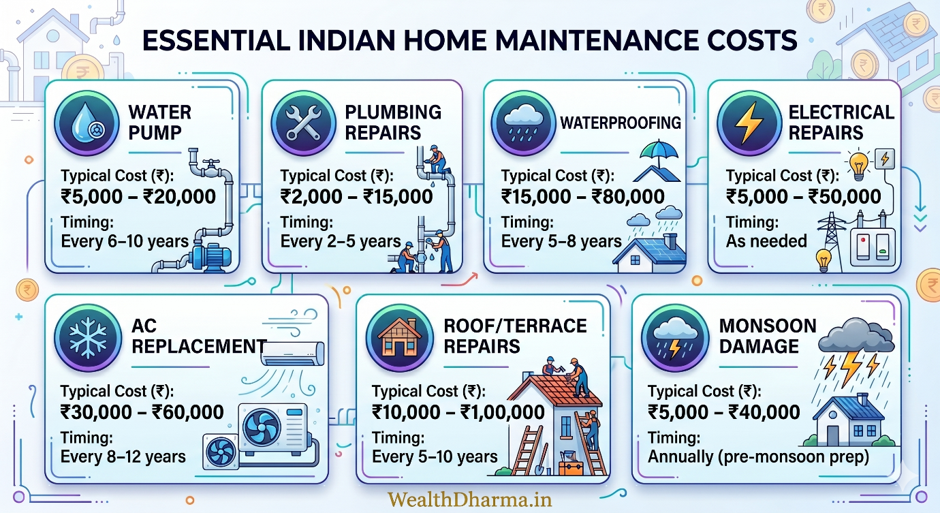

Common Home Repairs and Their Costs in India

The table below provides estimated repair costs across Indian cities. Costs vary based on your city, property type, contractor rates, and quality of materials chosen. Metro city rates are typically 30% to 50% higher than Tier 2 city rates for the same work.

| Repair Type | Estimated Cost (₹) | Typical Frequency | Risk Level |

| Water pump replacement | ₹5,000 – ₹20,000 | Every 6–10 years | High |

| Plumbing repairs | ₹2,000 – ₹15,000 | Every 2–5 years | High |

| AC servicing / replacement | ₹2,000 – ₹60,000 | Annual / every 10–12 yrs | Medium |

| Waterproofing (terrace/bathroom) | ₹15,000 – ₹80,000 | Every 5–8 years | High |

| Electrical repairs | ₹5,000 – ₹50,000 | As needed | Medium |

| Interior painting | ₹20,000 – ₹80,000 | Every 4–6 years | Low |

| Roof / terrace repairs | ₹10,000 – ₹1,00,000 | Every 5–10 years | High |

| Tile replacement | ₹5,000 – ₹40,000 | Every 10–15 years | Low |

| Door / window frame repair | ₹4,000 – ₹25,000 | Every 8–12 years | Medium |

| Overhead water tank | ₹3,000 – ₹15,000 | Every 8–15 years | Medium |

| Mould/seepage treatment | ₹8,000 – ₹40,000 | Post-monsoon, every few years | High |

Even two or three of these in a single year can cost ₹40,000 to ₹1,00,000 or more. A water pump failure, bathroom waterproofing, and a post-monsoon seepage treatment in the same year is not unusual — and not unaffordable if you have a fund in place.

How Much Should You Save? Two Practical Rules

There is no single formula that works for every homeowner. The right amount depends on your home’s value, age, location, climate, and maintenance history. Rather than using multiple conflicting formulas, focus on these two practical approaches.

Rule 1: The 1% Rule (Best for Most Homeowners)

| Home Value | Annual Saving Target | Monthly Saving Target |

| ₹25 lakh | ₹25,000 | ₹2,100 |

| ₹50 lakh | ₹50,000 | ₹4,200 |

| ₹75 lakh | ₹75,000 | ₹6,250 |

| ₹1 crore | ₹1,00,000 | ₹8,300 |

Set aside approximately 1% of your home’s current market value every year for maintenance and repairs.

If your home is more than 10 years old, located in a coastal region, or exposed to heavy monsoon conditions, consider increasing the target to 1.5%–2% annually. This is the most widely used rule because it automatically scales with the value of your property.

Rule 2: The Age-Based Rule

Think of your home like a car. The first few years are relatively inexpensive, but maintenance costs accelerate as major systems age. Understanding this lifecycle helps you save before large repair bills arrive.

Here is what typically happens as an Indian home ages:

| Age of House | What Typically Happens | Financial Implication |

| Year 1–3 | Minor paint touch-ups, fixing small leaks, grout issues. Society-covered snags if under builder warranty. | Low cost. Build the fund now while costs are minimal. |

| Year 4–6 | First plumbing issues. Water pump performance declining. Bathroom grout and tile problems begin. | First real repairs. ₹15,000–₹40,000 range. |

| Year 7–10 | Water pump replacement likely (where applicable). Bathroom waterproofing may fail. Electrical switchboard issues become more common. | Significant outlay. ₹30,000–₹80,000 in this window. |

| Year 11–15 | AC compressor replacement, overhead water tank issues, full bathroom waterproofing, interior repainting. | Major repair cycle. Budget ₹80,000–₹2,00,000. |

| Year 15–20 | Electrical rewiring may be required. Plumbing upgrades, window and door frame repairs, exterior repainting. | Heavy expenditure cycle. ₹1,50,000–₹5,00,000+. |

| Year 20+ | Structural repairs, complete waterproofing overhaul, plumbing replacement, and major system upgrades become more likely. | Ongoing significant annual investment required. |

These figures do not include interest earned. A sweep-in FD or liquid fund can add approximately 5–7% per year, increasing the fund’s value over time.

Why Starting Early Matters

A homeowner who saves ₹3,000 per month from the day they move into a new property can accumulate ₹1.8 lakh in just five years before interest. That amount can cover a complete waterproofing project, a major repainting cycle, a water pump replacement, or several plumbing and electrical repairs without touching the emergency fund or taking on debt.

The goal of a home repair fund is not to predict the e xact repair that will happen next. The goal is to ensure that when it does happen, the money is already waiting.

Where to Keep Your Home Repair Fund

The right account is one that is easily accessible, earns a reasonable return, and is kept completely separate from your regular savings. Here are the best options for Indian homeowners:

| Option | Best For | Return | Accessibility | WealthDharma Rating |

| Dedicated Savings Account | Getting started, small funds | 3–4% p.a. | Immediate | Good — simple and separate |

| Sweep-In FD Account | Most homeowners (ideal) | 5.5–7% p.a. | Within 1 day | Best — earns more, still accessible |

| Liquid Mutual Fund | Funds above ₹1 lakh | 6–7.5% p.a. | 1 working day | Good — slightly better returns |

| Recurring Deposit (RD) | Disciplined savers | 5–6.5% p.a. | On maturity (penalty to break) | Moderate — less flexible |

| Equity / Stock Market | Do NOT use | Variable | Variable | Not suitable — too volatile |

| Best recommendation for most Indian homeowners: Open a sweep-in FD account at your existing bank and label it your Home Repair Fund. It earns 5.5–7% interest (much better than a regular savings account) and sweeps money back automatically when you need it. Ask your bank: ‘I want to open a sweep-in FD linked to my savings account.’ Most major banks offer this — SBI, HDFC, ICICI, Axis, Kotak. |

Home Repair Fund vs Emergency Fund vs Home Insurance

| Feature | Home Repair Fund | Emergency Fund | Home Insurance |

| Purpose | Planned maintenance and repairs | Income disruption / medical crisis | Catastrophic structural damage |

| What triggers use | Pump fails, pipe leaks, waterproofing due | Job loss, hospitalisation, accident | Fire, flood, earthquake, lightning |

| What it does NOT cover | Catastrophic disasters | Routine home maintenance | Wear and tear, maintenance, pest damage |

| Who needs it | Every homeowner | Every earning individual | Every homeowner (mandatory for home loans) |

| Recommended amount | ₹50,000 – ₹2 lakhs+ | At least 6 months of expenses | Replacement cost of structure |

| Access speed | 1–2 days | Immediately | Insurance claim process (7–30 days) |

| Funded by | Monthly contributions | Monthly contributions | Annual premium (₹5,000–₹15,000/year) |

Why Apartment Owners Still Need a Home Repair Fund

Many apartment owners assume that monthly society or RWA maintenance charges significantly reduce their future repair costs. In reality, society maintenance charges primarily cover common infrastructure such as lifts, security, housekeeping, common-area lighting, external painting, and building-level maintenance.

Repairs inside your flat remain your responsibility. This includes plumbing, electrical work, waterproofing, internal painting, flooring, appliances, and most seepage-related repairs affecting your unit.

The bigger financial mistake is often made by owners of investment properties. A common pattern looks like this:

- Rent received: ₹25,000 per month

- Home loan EMI: ₹25,000 per month

- Result: Entire rent is used for EMI

On paper, the property appears self-sustaining. But when a ₹40,000 waterproofing bill, a ₹20,000 plumbing repair, or a ₹15,000 painting job arrives, there is no dedicated maintenance fund available.

Apartment owners face another reality: they inherit construction decisions they never made.

A homeowner building an independent house can personally choose materials, fittings, and workmanship standards. Apartment buyers do not have that luxury. They inherit whatever decisions were made by the builder years earlier.

Sometimes a builder saves a few rupees during construction by choosing a cheaper fitting, seal, washer, or waterproofing material. Years later, the homeowner may end up spending thousands—or even tens of thousands—fixing the consequences.

That is why smart homeowners assume that future repairs are not a possibility but a certainty.

Every property, whether self-occupied or rented out, requires ongoing maintenance. Rent should not be viewed as pure income. A portion should be set aside each month for future repairs and upkeep.

A useful WealthDharma mindset is this: Your tenant pays the EMI. You save for maintenance.

A property that generates rent but has no maintenance reserve is not truly paying for itself. Apartment owners need a home repair fund just as much as independent house owners. The repair categories may differ, but the need to prepare financially remains exactly the same.

Common Mistakes Indian Homeowners Make

Understanding what not to do is as important as knowing what to do. Here are the three most common financial mistakes homeowners make when repairs arrive:

Mistake 1: Using the emergency fund for home repairs

The emergency fund is your family’s financial lifeline if income stops. Using it for a home repair — however urgent — leaves your family exposed if a real emergency (job loss, medical crisis) follows. Always maintain separate funds for separate purposes.

Mistake 2: Borrowing from family or colleagues

Borrowing money from family creates financial and relational stress. It delays the repair of your financial habits. And it does not solve the underlying problem — you still have no fund the next time a repair arrives.

Mistake 3: Taking a personal loan for home repairs

Personal loan interest rates in India range from 10% to 24% per annum. A ₹50,000 repair funded by a 3-year personal loan at 16% costs approximately ₹68,000 in total. You paid ₹18,000 extra because you did not have a fund. That ₹18,000 is the price of not saving in advance.

| The cost of not saving: ₹50,000 repair paid from a home repair fund = ₹50,000. ₹50,000 repair paid via personal loan (16% for 3 years) = ₹68,000. ₹50,000 repair paid via credit card (40% for 1 year, unpaid) = ₹70,000. The home repair fund saves you ₹18,000–₹20,000 on a single repair. |

Practical Steps to Start Saving for Home Repairs Today

You do not need a large starting amount. You need a decision, a system, and consistency. Here are five concrete steps:

- Open a dedicated account today: Go to your bank’s app or branch and open a new savings account or sweep-in FD. Name it ‘Home Repair Fund’ or ‘House Maintenance.’ This single act of separation is the most important step.

- Decide your starting contribution : Use one of the three rules above. If unsure, start with ₹1,000–₹2,000 per month. You can always increase it. Starting small is infinitely better than not starting.

- Automate the transfer : Set a standing instruction or auto-debit for the 2nd or 3rd of every month — right after your salary credit. Automation removes the monthly decision entirely.

- Review every April (new financial year) : Check your fund balance. Consider whether your home has aged or whether repairs have reduced the balance. Adjust your monthly contribution accordingly.

- Replenish immediately after any withdrawal : After you use the fund for a repair, resume contributions at the same or a higher rate. Do not treat the post-repair period as a break — repairs rarely come alone.

Homeowners who feel the least financial stress are not necessarily the highest earners. They are the ones who planned ahead. A home repair fund is among the simplest and most effective personal finance decisions you can make.

Building a home repair fund is only one part of financial preparation. The other is reducing unnecessary repair costs. Every homeowner should keep a basic hand tool kit for routine maintenance and simple repairs. Read why a hand tool kit is one of the most practical gifts for new homeowners and newly married couples.

Conclusion: Protect Your Home. Protect Your Family.

Home repairs are not unexpected expenses. They are inevitable expenses with unpredictable timing. The homeowners who handle them calmly are the ones who saved before the repair arrived — not after.

Every Indian homeowner who has faced a sudden ₹40,000 repair bill without a fund knows the feeling: panic, stress, and regret that you did not prepare earlier. That feeling is optional. It disappears the moment you build a plan.

A home repair fund does not require a large income, a complex investment strategy, or a financial advisor. It requires a decision, a dedicated account, and a monthly transfer that happens automatically. Whether you save ₹1,000 or ₹5,000 per month, you are moving from reactive to proactive — from financial stress to financial calm.

| “A home repair fund is not just about fixing a house. It is about protecting your family’s financial stability when life delivers an unexpected repair bill.” — WealthDharma.in |

Finance is not just about growing wealth. It is also about protecting what you already own. A home repair fund may never be the most exciting financial goal. It will not make headlines, generate impressive returns, or become a conversation topic. But when a major repair arrives, it may be one of the most valuable financial decisions you ever made.

Start your home repair fund this month. Open a dedicated account. Set up an automatic transfer. Review it every April. Your future self — standing calmly in front of a contractor instead of panicking — will thank you.

Frequently Asked Questions (FAQs)

What is a home repair fund?

A home repair fund is a dedicated pool of savings set aside specifically for future home maintenance and repair expenses. It is kept completely separate from your emergency fund and used only for home-related repair needs such as plumbing, electrical work, waterproofing, pump replacement, and painting. Unlike an emergency fund, it is not for income disruption — it is specifically for the inevitable costs of maintaining a home.

How much should I save for home repairs each month?

Use the rule that fits your situation: (a) 1% of your home’s value per year divided by 12, (b) ₹3–5 per sq. ft of your home per year divided by 12, or (c) age-based — ₹1,000–₹2,000/month for new homes under 3 years, rising to ₹4,000–₹6,000/month for homes over 13 years. When in doubt, start with ₹2,000 per month and adjust upward annually.

Should home repairs come from my emergency fund?

No. Your emergency fund is your family’s protection against income loss — job loss, hospitalisation, or unexpected family needs. Using it for a home repair leaves your family exposed if a genuine emergency follows. A dedicated home repair fund keeps both purposes protected and intact.

Does my home insurance cover routine repairs?

No. Home insurance in India covers structural damage from fire, flood, earthquake, lightning, and burglary. It does not cover: plumbing wear and tear, pump breakdown, tile cracking, paint peeling, waterproofing failure, AC breakdown, or any maintenance-related repair. Home insurance and a home repair fund serve entirely different purposes — you need both.

Do apartment owners in India need a home repair fund?

Yes, absolutely. Society/RWA maintenance charges cover only common areas — staircases, lifts, external walls, common terraces, and common water tanks. All repairs inside your individual flat — plumbing, electrical, tiles, bathroom waterproofing, AC, internal painting, and door frames — are your personal responsibility. Apartment owners face repair costs as significant as independent house owners.

Where should I keep my home repair savings in India?

The best option for most Indian homeowners is a sweep-in FD account linked to your savings account. It earns 5.5–7% interest (significantly more than a regular savings account) and sweeps funds back to your account automatically when you need them. For funds above ₹1 lakh, a liquid mutual fund offers marginally better returns with similar accessibility.

What percentage of my home’s value should I save for maintenance and repairs?

A widely used rule is to save approximately 1% of your home’s current market value every year for maintenance and repair expenses. For example, a ₹50 lakh home would require a maintenance fund target of about ₹50,000 per year (around ₹4,200 per month). If your home is more than 10 years old, located in a coastal area, or exposed to heavy monsoon conditions, consider increasing the target to 1.5%–2% annually. The goal is not to predict specific repairs but to ensure funds are available when inevitable maintenance needs arise.